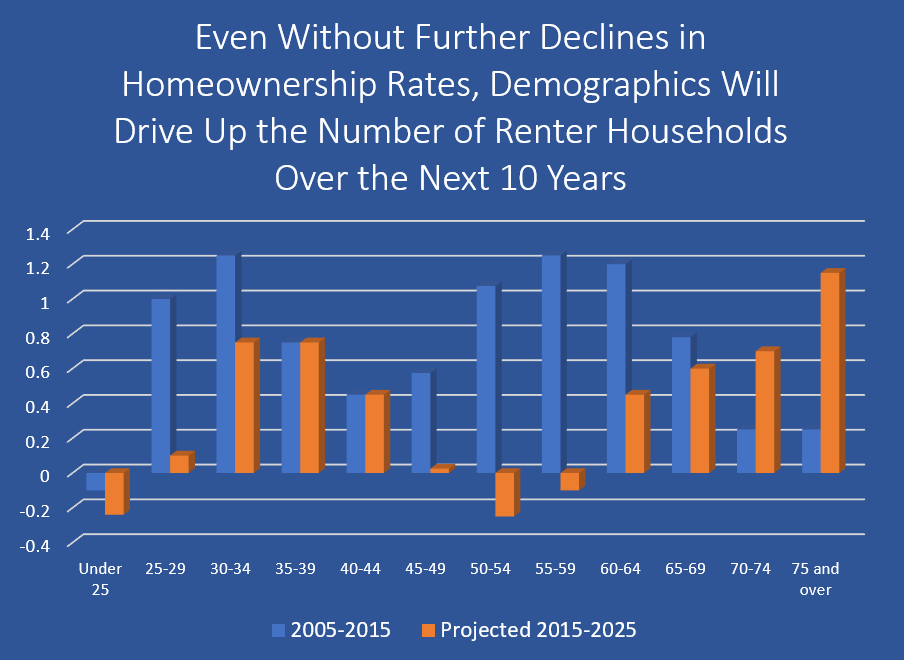

Since 2005, the number of renter households aged 50 and over has increased dramatically, jumping from 10 to nearly 15 million, and accounting for more than half of all renter growth over the past decade, as my colleague Dan McCue pointed out in a

recent post. This is not just a result of the large baby boom cohort passing age 50, but is also a distinct increase in the rate at which older adults are renting. As these trends are likely to continue, it’s concerning that the nation’s current supply of rental housing suitable to the needs and preferences of older renters is insufficient, particularly in relation to affordability and physical accessibility.

The baby boom cohort, now aged 50-69, is responsible for most of the increase in older renters. In the last decade, the boomer generation fully passed into the 50+ category, and going forward, this cohort will continue to drive up the number of renters in their 70s and beyond (

Figure 1).

Notes: Projected renter growth assumes constant homeownership rates by age, race, and household type. Constant rates are the average of rates from 2014 and 2015. Historical growth uses 3-year trailing annual averages to reduce volatility.

Sources: JCHS tabulations of US Census Bureau, Current Population Surveys and 2013 JCHS household growth projections.

Notes: Projected renter growth assumes constant homeownership rates by age, race, and household type. Constant rates are the average of rates from 2014 and 2015. Historical growth uses 3-year trailing annual averages to reduce volatility.

Sources: JCHS tabulations of US Census Bureau, Current Population Surveys and 2013 JCHS household growth projections.

However a growing older population is only part of the story: more than half the growth in older renters stems from a decline in homeownership and subsequent increase in the share of those 50 and over who rent, a legacy of the foreclosure crisis and recession. As our 2014 report on

housing for older adults noted, the homeownership rate for 50-64 year olds slipped 5 percentage points between 2005 and 2013—a larger drop than in the nation’s overall homeownership rate over that period. For these owners-turned-renters, transitioning back to homeownership can be especially difficult as retirement approaches: the imperative to save for retirement may take precedence over saving for a downpayment, while weak credit may make it difficult to obtain a mortgage. Though some may make their way back to homeownership despite these challenges, it is likely that the higher rentership rates among the boomer cohort will persist as the group ages.

While the recession pushed many into renting, other older homeowners are transitioning to renting as a choice. For these owners, rentals may offer a smaller, more cost-effective option that demands less time, physical effort, and money to maintain. As mobility limitations increase with age, older owners also turn to renting to obtain more accessible housing, with features like single-floor living, no-step entries into the unit, walk-in showers, and other

universal design elements. As the large baby boom population enters the 70-plus age range in the next decade, we can expect a swell in the number of older renters seeking accessibility features that can enhance safety in the home, independence, and quality of life.

It remains to be seen whether baby boomers will elect to make these moves earlier than their predecessors. With growing interest in walkable communities, proximity to transit, and back-to-the-cities living, we may see earlier turns to renting as a choice. But even if not, the sheer growth in older households and the falloff in owning compared to previous generations at the same age indicates strong growth in older renter households going forward, even absent further declines in homeownership.

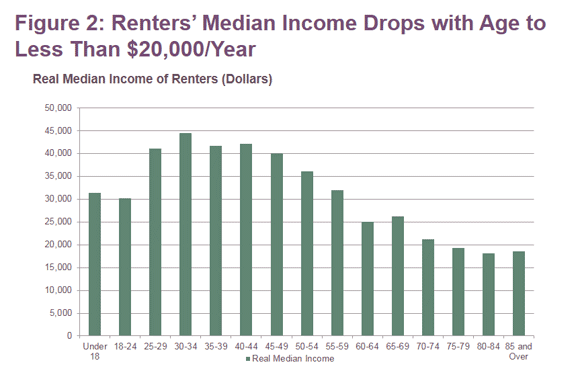

The question then is whether the nation’s supply of rental units is suited to the needs and preferences of older renters. Like renters in general, older renters have lower median incomes than their home-owning counterparts. But since incomes decline in retirement, older renters also have lower median incomes than renters in general (

Figure 2). Lower incomes leave a significant share of older renters vulnerable to housing cost burdens. Indeed, 55 percent of renters aged 65 and over are cost burdened, spending more than 30 percent of their income on housing, including 30 percent who spend more than half their income on housing. Older cost-burdened renters typically spend less on food, healthcare, and transportation – and for those in their 50s and early 60s, save less for retirement, threatening financial security down the road.

Notes: Real Median Incomes are as of 2014 and have been adjusted for inflation using the CPI-U for all items.

Source: JCHS tabulations of US Census Bureau, 2015 Current Population Survey.

Notes: Real Median Incomes are as of 2014 and have been adjusted for inflation using the CPI-U for all items.

Source: JCHS tabulations of US Census Bureau, 2015 Current Population Survey.

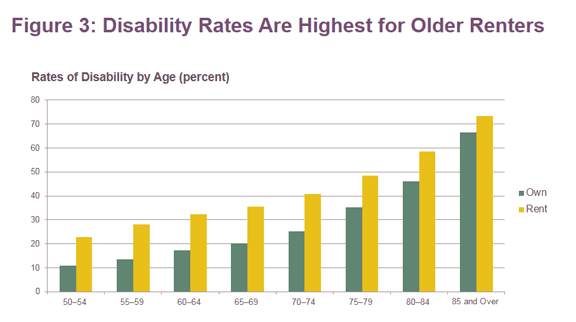

As noted below, older renters are more likely to have disabilities than younger renters, as well as homeowners of the same age (

Figure 3). Yet the supply of accessible units is limited; less than 1 percent of US rentals include five basic universal design features (a no-step entry, single-floor living, wide hallways and doors, electrical controls reachable from wheelchair height, and lever-style handles on doors and faucets). Units in newer, larger buildings are apt to offer more, yet still, just 6 percent of units in buildings constructed 2003 and later, and 11 percent of units in larger apartment buildings with 20 or more units, offer all five of these features. And newer rentals tend to command higher rents, leaving them out of reach to lower-income households with disabilities.

Notes: For individuals age 15 and older, a disability is defined as a hearing, vision, cognitive, ambulatory, self-care, or independent living difficulty. White households are non-Hispanic. Includes non-group quarters population only.

Source: JCHS tabulations of US Census Bureau, 2012 American Community Survey.

Notes: For individuals age 15 and older, a disability is defined as a hearing, vision, cognitive, ambulatory, self-care, or independent living difficulty. White households are non-Hispanic. Includes non-group quarters population only.

Source: JCHS tabulations of US Census Bureau, 2012 American Community Survey.

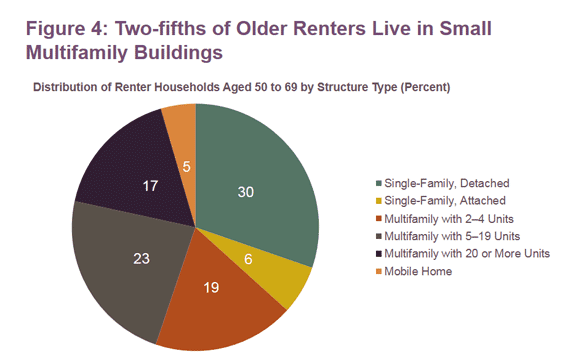

Indeed, older adults seeking housing that is both affordable and accessible face particular challenges. The current affordable stock tends to be older and located in smaller multifamily buildings that are the least likely of any rentals to offer accessibility features. Two-fifths of renter households in their 50s and 60s live in apartments in small buildings with 2-9 units (

Figure 4), which are among the oldest and least accessible units in the entire rental stock. Meanwhile, over a third live in single-family rentals whose accessibility varies widely by region, with renters in the Northeast and Midwest at particular disadvantage for single-floor living.

Source: JCHS tabulations of 2013 American Housing Survey, US Department of Housing and Urban Development

Source: JCHS tabulations of 2013 American Housing Survey, US Department of Housing and Urban Development

In addition to lower-cost and more accessible rentals, we will likely see an increase in demand for rentals with services that enhance older adults’ quality of life. Many older adults are not in need of assisted living or skilled nursing care, but could benefit from services such as transportation, laundry, or housekeeping that can support independent living into older ages. For lower-income adults, service-enhanced housing, where services are provided onsite, or service networks that support older renters scattered in multiple locations, can fill a role that their higher income peers can obtain through “

village” membership organizations or the more independent portions of continuing care retirement communities.

With renters 50 and over now comprising a third of the renter population – and renters 40 and over representing fully half – now is the time to consider the suitability of the nation’s rental stock for older renters and begin to address its shortfalls in accessibility and affordability. There is an urgent need to create more accessible units, through new construction or retrofit, suitable and affordable to older adults. This is particularly true for the oldest cohort, which has both the lowest median income of all renters and the highest rate of disability, and which will grow in size as the baby boomer generation ages into their 70s. Meanwhile, service-enhanced rental housing can play a critical role in extending independence and quality of life for those lower-income renters who do not need skilled nursing care or assisted living, but who could benefit from services that support independent living.

Notes: Real Median Incomes are as of 2014 and have been adjusted for inflation using the CPI-U for all items.

Source: JCHS tabulations of US Census Bureau, 2015 Current Population Survey.

As noted below, older renters are more likely to have disabilities than younger renters, as well as homeowners of the same age (Figure 3). Yet the supply of accessible units is limited; less than 1 percent of US rentals include five basic universal design features (a no-step entry, single-floor living, wide hallways and doors, electrical controls reachable from wheelchair height, and lever-style handles on doors and faucets). Units in newer, larger buildings are apt to offer more, yet still, just 6 percent of units in buildings constructed 2003 and later, and 11 percent of units in larger apartment buildings with 20 or more units, offer all five of these features. And newer rentals tend to command higher rents, leaving them out of reach to lower-income households with disabilities.

Notes: Real Median Incomes are as of 2014 and have been adjusted for inflation using the CPI-U for all items.

Source: JCHS tabulations of US Census Bureau, 2015 Current Population Survey.

As noted below, older renters are more likely to have disabilities than younger renters, as well as homeowners of the same age (Figure 3). Yet the supply of accessible units is limited; less than 1 percent of US rentals include five basic universal design features (a no-step entry, single-floor living, wide hallways and doors, electrical controls reachable from wheelchair height, and lever-style handles on doors and faucets). Units in newer, larger buildings are apt to offer more, yet still, just 6 percent of units in buildings constructed 2003 and later, and 11 percent of units in larger apartment buildings with 20 or more units, offer all five of these features. And newer rentals tend to command higher rents, leaving them out of reach to lower-income households with disabilities.

Notes: For individuals age 15 and older, a disability is defined as a hearing, vision, cognitive, ambulatory, self-care, or independent living difficulty. White households are non-Hispanic. Includes non-group quarters population only.

Source: JCHS tabulations of US Census Bureau, 2012 American Community Survey.

Indeed, older adults seeking housing that is both affordable and accessible face particular challenges. The current affordable stock tends to be older and located in smaller multifamily buildings that are the least likely of any rentals to offer accessibility features. Two-fifths of renter households in their 50s and 60s live in apartments in small buildings with 2-9 units (Figure 4), which are among the oldest and least accessible units in the entire rental stock. Meanwhile, over a third live in single-family rentals whose accessibility varies widely by region, with renters in the Northeast and Midwest at particular disadvantage for single-floor living.

Notes: For individuals age 15 and older, a disability is defined as a hearing, vision, cognitive, ambulatory, self-care, or independent living difficulty. White households are non-Hispanic. Includes non-group quarters population only.

Source: JCHS tabulations of US Census Bureau, 2012 American Community Survey.

Indeed, older adults seeking housing that is both affordable and accessible face particular challenges. The current affordable stock tends to be older and located in smaller multifamily buildings that are the least likely of any rentals to offer accessibility features. Two-fifths of renter households in their 50s and 60s live in apartments in small buildings with 2-9 units (Figure 4), which are among the oldest and least accessible units in the entire rental stock. Meanwhile, over a third live in single-family rentals whose accessibility varies widely by region, with renters in the Northeast and Midwest at particular disadvantage for single-floor living.

Source: JCHS tabulations of 2013 American Housing Survey, US Department of Housing and Urban Development

In addition to lower-cost and more accessible rentals, we will likely see an increase in demand for rentals with services that enhance older adults’ quality of life. Many older adults are not in need of assisted living or skilled nursing care, but could benefit from services such as transportation, laundry, or housekeeping that can support independent living into older ages. For lower-income adults, service-enhanced housing, where services are provided onsite, or service networks that support older renters scattered in multiple locations, can fill a role that their higher income peers can obtain through “village” membership organizations or the more independent portions of continuing care retirement communities.

With renters 50 and over now comprising a third of the renter population – and renters 40 and over representing fully half – now is the time to consider the suitability of the nation’s rental stock for older renters and begin to address its shortfalls in accessibility and affordability. There is an urgent need to create more accessible units, through new construction or retrofit, suitable and affordable to older adults. This is particularly true for the oldest cohort, which has both the lowest median income of all renters and the highest rate of disability, and which will grow in size as the baby boomer generation ages into their 70s. Meanwhile, service-enhanced rental housing can play a critical role in extending independence and quality of life for those lower-income renters who do not need skilled nursing care or assisted living, but who could benefit from services that support independent living.

Source: JCHS tabulations of 2013 American Housing Survey, US Department of Housing and Urban Development

In addition to lower-cost and more accessible rentals, we will likely see an increase in demand for rentals with services that enhance older adults’ quality of life. Many older adults are not in need of assisted living or skilled nursing care, but could benefit from services such as transportation, laundry, or housekeeping that can support independent living into older ages. For lower-income adults, service-enhanced housing, where services are provided onsite, or service networks that support older renters scattered in multiple locations, can fill a role that their higher income peers can obtain through “village” membership organizations or the more independent portions of continuing care retirement communities.

With renters 50 and over now comprising a third of the renter population – and renters 40 and over representing fully half – now is the time to consider the suitability of the nation’s rental stock for older renters and begin to address its shortfalls in accessibility and affordability. There is an urgent need to create more accessible units, through new construction or retrofit, suitable and affordable to older adults. This is particularly true for the oldest cohort, which has both the lowest median income of all renters and the highest rate of disability, and which will grow in size as the baby boomer generation ages into their 70s. Meanwhile, service-enhanced rental housing can play a critical role in extending independence and quality of life for those lower-income renters who do not need skilled nursing care or assisted living, but who could benefit from services that support independent living.

About the author

Neighborhood Ventures